【译者按】CPA财会翻译网的创办方——上海汇英企业管理咨询有限公司拥有20年财务报表中英文翻译经验,根据本公司译员对财务报表的常年研习并参照国际财务报告准则的语言分类规范,针对我国企业会计准则规定的会计科目目录,CPA财会翻译网已独立开发了标准化的财务报表分类项目中英文对照表,以确保财务报表术语翻译准确,符合国际财务报告语言的规范要求。

利润表定义

Definition of Income Statement

Definition of Income Statement

利润表是反映企业在一定会计期间(如季度或年度)经营成果的会计报表。企业一定会计期间的经营成果既可能表现为盈利,也可能表现为亏损,因此,利润表也被称为损益表。利润表主要是根据“收入-费用=利润”这一会计等式,依照一定的分类标准和顺序,将企业一定会计期间的各种收入、费用支出和直接计入当期利润的利得和损失进行适当分类、排列而成的。由于表内数据是说明某一期间的情况,利润表属于动态报表。

The income statement is a financial statement that reports the results of operations of an entity during a specific accounting period such as a quarter or a year. It is also called a profit and loss (P&L) statement because the entity’s operating results for a specific accounting period may be presented in profit or loss. Based on the accounting equation, Revenue - Expenses = Profit and the specified criteria for classification and ordering of items, the income statement is prepared by classifying and listing appropriately all the revenues, expenses, gains and losses directly included in the income statement for the current period. As the information in the income statement depicts the conditions over a specific period of time, the income statement is a dynamic statement.

利润表具有以下作用:

- (1)利润表反映了企业经营业绩的主要来源和构成,有助于财务报表使用者判断净利润的质量及其风险,有助于使用者预测净利润的持续性,从而帮助其作出正确的决策。

- (2)通过利润表,可以从总体上了解企业收入、成本和费用、净利润(或亏损)的实现及构成情况,帮助使用者全面了解企业的经营成果。

- (3)通过利润表提供的不同时期的比较数字,使用者可以分析企业的获利能力及利润的未来发展趋势,了解投资者投入资本的保值增值情况,从而为其作出经济决策提供依据。

- (4)利润表中的信息与资产负债表中的信息相结合,还可以为财务分析提供基本资料,可以反映企业的资金周转情况、盈利能力和水平,便于报表使用者判断企业未来的发展趋势并作出经济决策。

The income statement has the following functions:

- (1) The income statement reflects the main sources and components of an entity's operating performance, which assist financial statement users in judging the quality of net income and its risks, and in predicting the sustainability of net income, thus making their right decisions.

- (2) Through the income statement, users can have an overall view of the realization and composition of revenues, costs and expenses, and net income (or loss) of an entity, thus obtaining a comprehensive understanding of the entity’s operating results.

- (3) Through the comparative figures provided by the income statement over time, users can analyze the entity's profitability and future trends of its earnings, and learn about the capital maintenance and value increase of investments contributed by investors, thus providing them with a basis for making economic decisions.

- (4) The information in the income statement combined with the information in the balance sheet can also provide basic information for financial analysis, which can reflect the entity’s financial turnover, profitability and earnings level, and facilitate financial statement users to judge the entity’s future development trend, thus making economic decisions.

利润表格式

Formats of Income Statement

Formats of Income Statement

利润表的格式主要有单步式利润表和多步式利润表两种。

There are two primary formats of income statements: single-step income statements and multiple-step income statements.

单步式利润表是将当期所有的收入列在一起,将所有的费用列在一起,两者相减得出当期净利润。该报告格式直观、简单,避免了项目分类上的困难,但其提供的信息量较少,不利于报表使用者分析企业经营业绩的主要来源和构成,不利于比较不同单位之间的利润构成,也不利于预测企业未来的盈利能力。

In the single-step income statement, all the revenues and expenses for the current period are laid out separately in two sections where total expenses are subtracted from total revenues to arrive at net income (or loss) for the current period. This reporting format is straightforward and simple without complexities in categorizing line items, but it provides less information, which is not good for financial statement users to analyze the main sources and components of the entity’s operating results, to compare the components of profit or loss between different entities, or to predict the the entity’s future profitability.

多步式利润表是通过对收入、费用按性质加以归类,按利润形成的主要环节列示一些中间性利润指标,分步计算当前净损益。这种报告格式虽然计算较为复杂,但是提供的信息量丰富,不仅可以反映企业最终的经营成果,而且还能反映不同业务的盈亏水平,可以反映企业经营成果的不同来源和形成过程,便于报表使用者分析企业净利润增减变动原因,评价净利润质量及其风险,有助于预测企业未来的盈利能力。

In the multiple-step income statement, net income or loss for the current period is calculated on a step-by-step basis by grouping revenues and expenses based on their nature and presenting a number of interim profit indicators according to main steps for profit realization. Although this reporting format is more complex to calculate, it provides sufficient information to reflect not only the final operating results of an entity, but also the profit and loss levels of different business transactions, to give a view of the different sources and formation processes of the entity's operating results, thus facilitating the users of financial statements to analyze the reasons for the changes (increases or decreases) in the net income of the entity, to evaluate the quality of net income and its risks, and to help predict the future profitability of the entity.

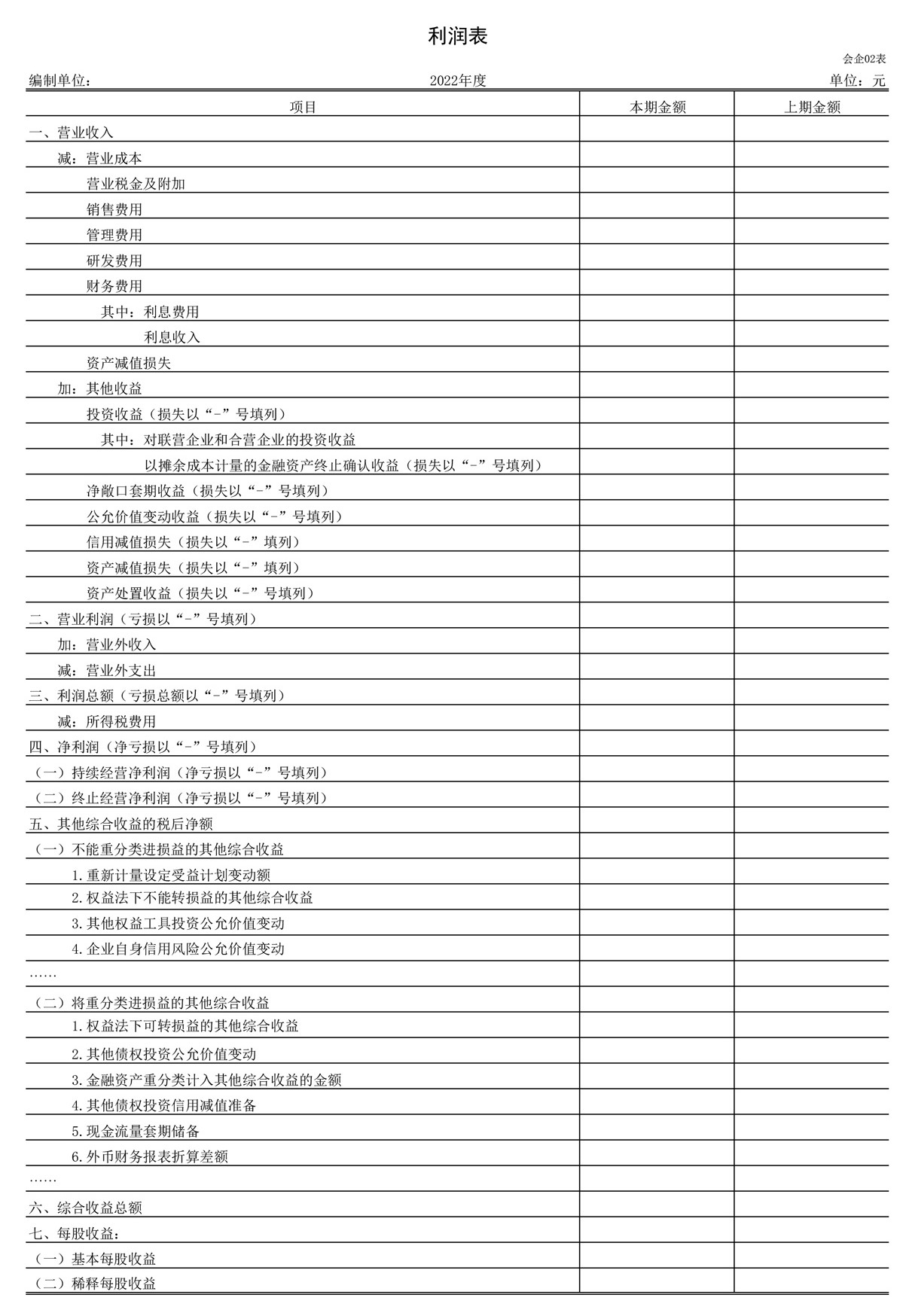

我国企业的利润表采用多步式的格式(见利润表样式)。多步式利润表分为四个层次:第一层次计算营业利润,第二层次计算利润总额,第三层次计算净利润,第四层次计算综合收益总额。

- (1) 营业利润: 营业利润=营业收入-营业成本-营业税金及附加-销售费用-管理费用-财务费用-资产减值损失+公允价值变动收益(-公允价值变动损失)+投资收益(-投资损失)

- (2) 利润总额: 利润总额=营业利润+营业外收入-营业外支出

- (3) 净利润: 净利润=利润总额-所得税费用

- (4) 综合收益总额: 综合收益总额=净利润+其他综合收益

The Chinese enterprises usually adopt the multiple-step format for their income statements (see the Sample of Income Statement below). The multiple-step income statement is divided into four levels: at the first level, operating profit is calculated; at the second level, total profit is calculated; at the third level, net income is calculated, and at the fourth level, total comprehensive income is calculated. The formulas for calculating the above four levels are illustrated as follows:

- (1) Operating profit/loss: Operating profit = Operating revenue - Operating costs – Operating taxes and surcharges - Selling expenses - Administrative expenses – Financial expenses - Impairment loss of assets + Income from changes in fair value (- Losses on changes in fair value) + Income from investments (- Losses on investments)

- (2) Total profit/loss (Income/loss before income tax): Total profit = Operating profit + Non-operating revenue - Non-operating expenses

- (3) Net income/loss: Net profit = Total profit - Income tax expense

- (4) Total comprehensive income: Total comprehensive income = Net income + Other comprehensive income

利润表样式

Sample of Income Statement

Sample of Income Statement

以上利润表|损益表中英文翻译由CPA财会翻译网提供并翻译,版权所有,不得转载。